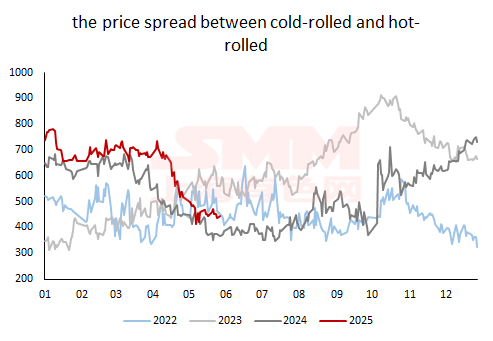

- Mid-May: Cold-hot price spread stopped falling and stabilized

According to SMM data, as of May 30, the average cold-hot price spread nationwide was 443 yuan/mt, down 1.0% WoW from the weekly average, and down 27.5% MoM from the monthly average.

However, recently, the cold-hot price spread, which had been falling rapidly since early April, finally showed signs of stopping falling and stabilizing. According to the data, the average cold-hot price spread in late May was 455 yuan/mt, up 1.6% WoW from the first half of the month.

- Tariff War Hits Pause Button, Golden Window Period Supports Slowdown in Price Declines for Cold-rolled Steel Products

On May 12, a joint statement was issued following the China-US economic and trade talks in Geneva, announcing a significant reduction in bilateral tariff levels between China and the US: The US will (1) revise the ad valorem tariffs imposed on Chinese goods (including goods from the Hong Kong Special Administrative Region and the Macao Special Administrative Region) as stipulated in Executive Order 14257 issued on April 2, 2025. Specifically, 24% of these tariffs will be suspended for the initial 90-day period, while the remaining 10% of tariffs on these goods will be retained for potential imposition in accordance with the provisions of the executive order; (2) cancel the additional tariffs imposed on these goods under Executive Order 14259 issued on April 8, 2025, and Executive Order 14266 issued on April 9, 2025.

China will (1) make corresponding revisions to the ad valorem tariffs imposed on US goods as stipulated in Announcement No. 4, 2025 of the Customs Tariff Commission (CTC). Specifically, a 24% tariff will be suspended for the initial 90-day period, while the remaining 10% tariff on these goods will be retained, and the tariff hikes imposed on these goods in accordance with Announcement No. 5 and No. 6, 2025 of the CTC will be cancelled; (2) take necessary measures to suspend or cancel non-tariff countermeasures against the US that have been in place since April 2, 2025.

The tariff war has been put on hold, and a 90-day golden window for exports has opened. Wang Jianguo, Vice President of Midea Group and President of the Smart Home Business Group, stated in an interview that within the 90-day period, the tariff on most home appliances exported from China to the US will be 55% (25% + 20% + 10%). In comparison to April 1 this year, only a 10% tariff is newly imposed. It is expected that the vast majority of home appliances produced in China will resume shipments.

According to SMM's latest survey, after the conclusion of tariff negotiations, several home appliance enterprises have resumed order flows heading to the US. Some enterprises have reported tight cabin or container availability, which has somewhat limited shipping schedules. However, they remain relatively optimistic about the 90-day golden export period.

The reduction in manufacturing export costs and the improvement in order situations, which are important branches of demand in the cold-rolled steel industry, have largely provided support for cold-rolled steel prices, ending the continuous decline in the price spread between cold-rolled and hot-rolled steel.

- June: The cold-rolled and hot-rolled price spread is expected to see a slight recovery.

Based on the profitability of steel mills as reported by SMM, due to the significant decline in cold-rolled steel prices in the earlier period, the immediate profitability of cold-rolled steel has now fallen below the critical point, while the profitability of hot-rolled steel remains around 100 yuan/mt. In the short term, steel mills have relatively low enthusiasm for producing cold-rolled steel, resulting in low production volumes. On the demand side, the reduction in tariffs, combined with stimulus policies targeting manufacturing products such as trade-in policies and national subsidies in China, are expected to support manufacturing demand, maintaining strong resilience amidst increasing seasonal impacts. It is anticipated that the rate of decline in demand for both cold-rolled and hot-rolled steel will be relatively slow in June.

Overall, the production pressure for cold-rolled steel in June is expected to be lower than that for HRC. The current cold-rolled and hot-rolled price spread has narrowed to a relatively low level compared to the same period in recent years, with the price spread in some regions approaching the cost line, making further downward adjustments difficult. It is expected that the cold-rolled and hot-rolled price spread will see a slight recovery in June.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)